Rising crude demand set to boost the year ahead

By early December, average crude tanker earnings hovered around $36,000/day. Suezmax and Aframax have showed the most resilient segments. Seasonal improvements that typically bolster the fourth quarter have yet to fully materialize. However, shipbrokering house Fearnleys forecasts a potential rate rally in Q1, driven by seasonal shifts – offering a more optimistic outlook for the months ahead.

OPEC+ decided to extend its production cuts until March 2025, reflecting a cautious approach to market rebalancing. The an- ticipated easing of these cuts in March is expected to positively impact the tanker market.

Despite not reaching the peak rates recorded in the same period last year (Q4), 2024 has been a positive year for the tanker sector overall, buoyed by strong growth in Chinese imports. In Novem- ber, seaborne Chinese crude oil imports rose by 3% month-on- month to an estimated 9.9 million barrels per day. This marked an 8% year-on-year increase, according to Clarksons.

Chinese exports growth crucial to a promising 2025

Lower Middle Eastern crude prices encouraged stockpiling, supporting this growth. Additionally, Chinese product exports surged by 30% month-on-month to 0.9 million barrels per day, with gasoline exports rebounding as refiners maximized profits ahead of export tax rebate changes in December.

Looking ahead, the crude tanker sector holds promise for 2025.

Crude demand is projected to grow by 2.3%, while fleet expansion remains limited to just 1.2%, according to Clarksons. This favourable supply-demand dynamic could pave the way for stronger earnings and a well-balanced market, setting the stage for a positive outlook in the coming year.

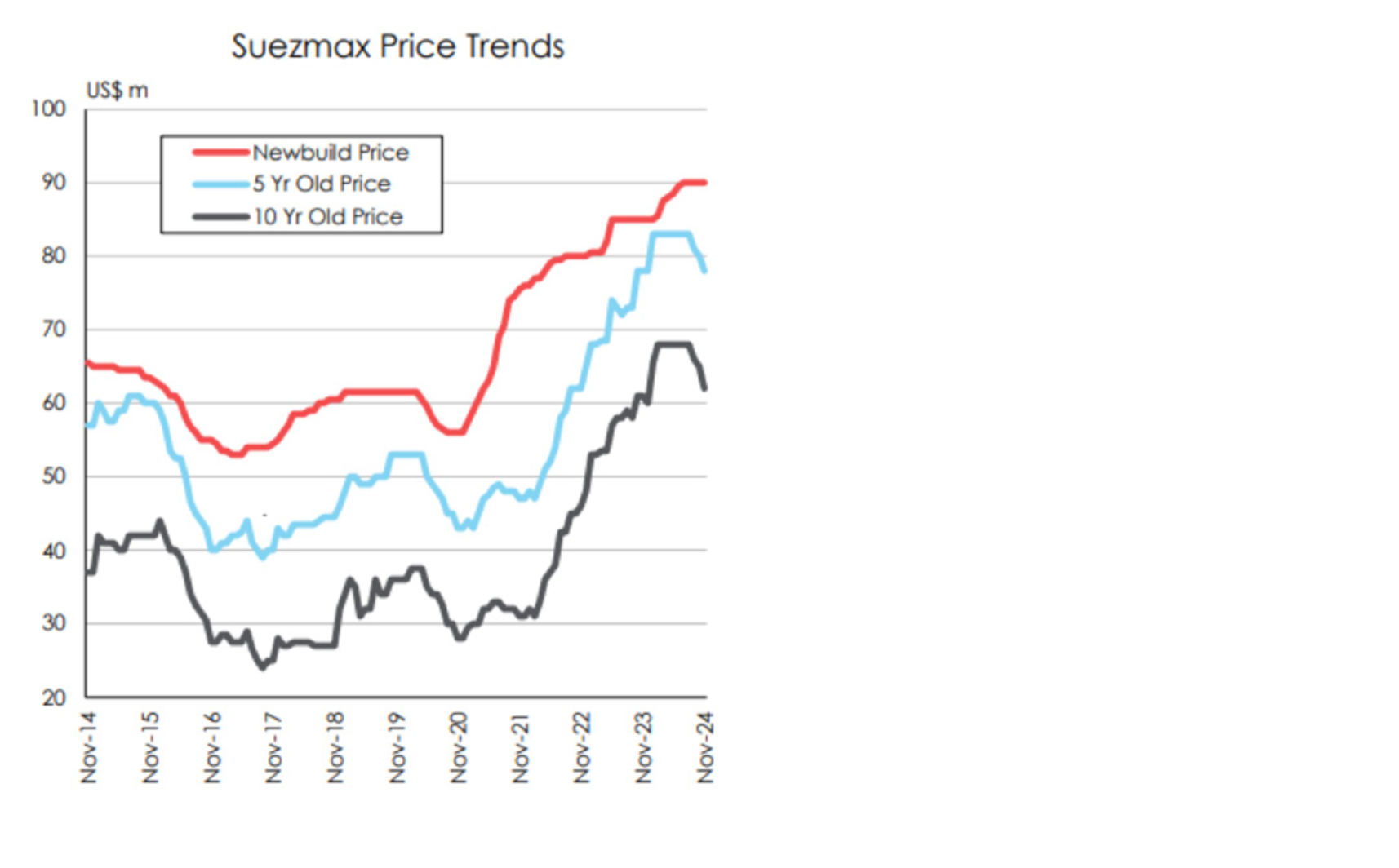

Source: Clarksons research