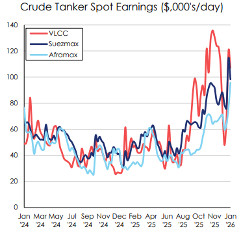

Earnings remain elevated despite short-term volatility

Crude tanker markets remained structurally strong throughout January, despite periods of short-term volatility. While earnings softened briefly following late-2025 highs, average rates remained well above historical levels, supported by high global production, elevated seaborne volumes and ongoing inefficiencies linked to sanctions and trade fragmentation. The ClarkSea Index fluctuated during the month but stayed comfortably above long-term averages, underlining that recent pullbacks reflected normalisation rather than a deterioration in fundamentals. An oversupplied oil market continues to support tanker utilisation, even as crude prices remain capped by surplus conditions.

Geopolitics and China shape tanker demand

Geopolitical developments were a key driver of sentiment and volatility. Ongoing tensions involving Iran added a persistent risk premium, particularly in the Middle East Gulf, where fixing activity periodically tightened tonnage availability and pushed earnings sharply higher. While no major physical disruption occurred, uncertainty around Iranian exports and US policy toward sanctioned producers kept charterers cautious and owners supported. China remained central to the tanker outlook, with its sourcing decisions determining whether sanctioned barrels continued to flow via non-compliant tonnage or were replaced by compliant crude from alternative suppliers.

Venezuela’s return introduces structural tightening

Developments in Venezuela marked a meaningful structural shift for the tanker market. The US-led move to re-market Venezuelan crude through compliant channels, with Vitol and Trafigura authorised to market up to 50 million barrels, represents a transition away from opaque trade flows that have historically relied on older grey-fleet vessels. Initial cargoes moved to the US Gulf and Caribbean storage hubs, with further exports expected as bottlenecks clear. Over time, this shift has the potential to tighten effective tanker supply through the erosion of non-compliant tonnage, while redirecting volumes in ways that support Aframax, Suezmax and potentially VLCC demand depending on destination.

Structural factors support the medium-term outlook

Overall, January reinforced the view that tanker market strength is increasingly underpinned by structural rather than cyclical factors. High production levels, compliance-driven trade re-routing, sanctions enforcement and the potential use of floating storage in an oversupplied oil market all point toward sustained utilisation. While short-term rate volatility is likely to persist, the month’s developments strengthen the medium-term outlook for crude tanker earnings and asset values.

Sources: Clarksons, MB Shipbrokers, Bloomberg, Reuters, TradeWinds