Sustained tensions and elevated risk expected for the time ahead

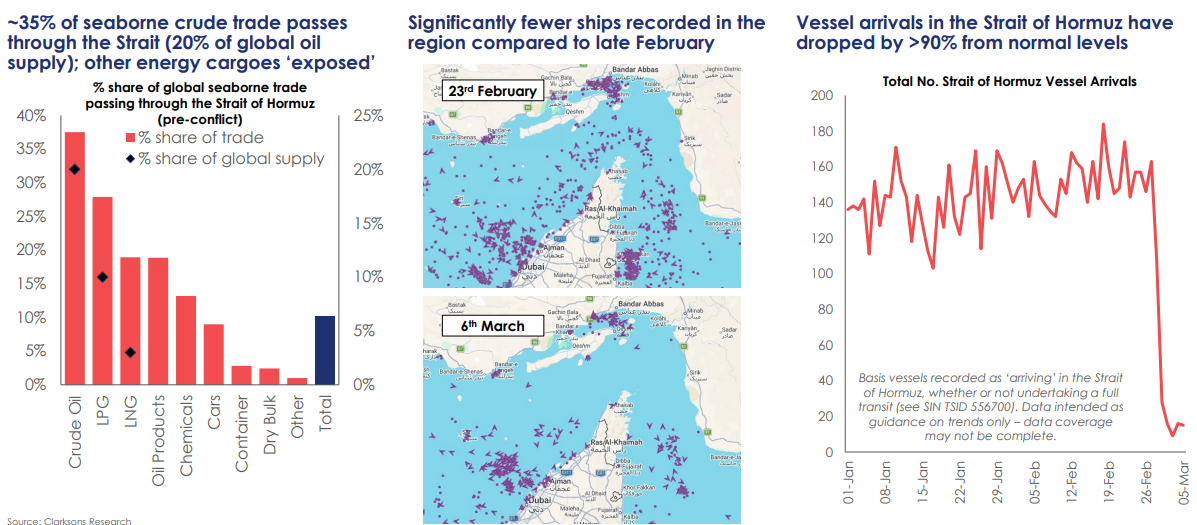

The escalation of tensions between the US, Israel and Iran has significantly increased geopolitical risk in the Middle East, particularly around the Strait of Hormuz. This waterway is one of the world’s most important energy chokepoints, handling roughly 20% of global oil trade and a significant share of global LPG flows.

Recent attacks on vessels, threats to regional energy infrastructure, and rising military tensions have led to a sharp reduction in ship traffic through the strait, as vessels delay transit or wait for clearer security conditions.

For shipping markets, the implications differ across segments.

Tanker market

The tanker market is currently our most directly affected segment and has seen the most positive immediate impact. Disruptions in the Strait of Hormuz increase operational risk and cause delays, rerouting and waiting times for vessels. This reduces the effective availability of ships, often referred to as “fleet inefficiency”, which tends to push freight rates higher, as recorded in previous weeks.

In addition, alternative export routes from the Middle East – such as Saudi Arabia’s East-West pipeline to the Red Sea – cannot fully replace the region’s normal export capacity through the Gulf. As a result, disrupted Middle Eastern volumes, may increasingly need to be replaced by cargoes from other regions such as West Africa and the Americas. These replacement trades normally involve significantly longer sailing distances as the majority of the oil imports are heading to East Asia, which ties vessels up for longer periods. In practice, this reduces the effective availability of ships in the market and tends to support freight rates in the tanker segment.

LPG market

A significant share (30%) of global LPG exports are flowing through the strait, and disruptions to regional supply can tighten cargo availability. At the same time, alternative supply – particularly from the United States – may need to replace disrupted Middle Eastern volumes. This could increase transport distances (ton-miles) for LPG cargoes, supporting LPG shipping demand and vessel earnings.

The conflict has led to several cancelled loadings, with a number of VLGCs redirecting towards the United States amid uncertainty regarding the potential duration of military action.

Overall, the LPG shipping market is expected to benefit from the conflict as long as any major disruption to the Strait of Hormuz remains temporary. However, a prolonged closure of the strait could lead to global LPG shortages, as other exporting regions would struggle to fully replace the potential loss of Middle Eastern supply.

Car carrier market

The impact on the car carrier (PCTC) market is more indirect, but the sector still has meaningful exposure to the Strait of Hormuz. Approximately 9% of global seaborne car trade transits through the strait, equivalent to roughly 3.3 million Cars annually, primarily from China, Japan, the United States, South Korea and Europe to markets such as Saudi Arabia and the UAE.

Following the escalation of the conflict, several operators have suspended bookings to the Persian Gulf, and vessels currently in the region are facing delays and scheduling uncertainty, which acts as a supporting factor for the segment earnings.

In the short term, the main impact is therefore operational disruption rather than a structural change in market fundamentals. If the disruption persists, vessels currently deployed in the Gulf may be redeployed to other trades, temporarily increasing vessel availability in other regions. However, once transit conditions normalize, vehicle trade flows to the Gulf are expected to resume.

Overall assessment

While there are currently no signs of an imminent truce between Iran and the US/Israel, we find it unlikely that the Strait of Hormuz will remain effectively closed for an extended period. Iran itself relies heavily on oil exports through the strait to generate revenue for its economy and to fund its military operations, making a prolonged shutdown economically unsustainable.

That said, we expect heightened tensions and elevated risk levels in the region to persist for some time. This is likely to keep insurance premiums and rates elevated, while encouraging charterers to source replacement cargoes from other regions to compensate for disrupted Middle Eastern volumes.

Under such a scenario, tanker and LPG markets are likely to benefit highly from increased disruption, longer trade routes and operational inefficiencies, all of which tighten the effective supply of vessels. The car carrier market, by contrast, is expected to remain largely unaffected, with the primary impact limited to temporary scheduling disruptions.

For shipping markets, the key factor is therefore the duration of the closure. Short-term disruptions typically support freight rates, whereas a prolonged closure of the Strait of Hormuz would eventually reduce cargo volumes and become negative for shipping markets overall, as other regions cannot fully replace the lost Middle Eastern supply.

Looking slightly ahead, we can also observe that countries are increasingly drawing on their oil and gas inventories to replace lost volumes. If the conflict proves short-lived, this could lead to a period of stronger trade afterwards as inventories will need to be rebuilt. As such, lower inventory levels may support increased trade activity in the coming years.