Chinese vehicle exports remain the core demand driver

PCTC markets were supported throughout January by continued strength in Chinese vehicle exports, which remain the single most important structural driver for global car carrier demand. China’s exports of cars and vans increased by more than 20% year on year in 2025, driven primarily by rapid growth in electric vehicle and plug-in hybrid shipments as manufacturers redirected excess domestic capacity toward overseas markets. Export volumes surpassed 7 million units, reinforcing China’s role as the dominant marginal supplier of vehicles to global markets. Still, what mutes the PCTC market is the increased fleet growth over the next two years,

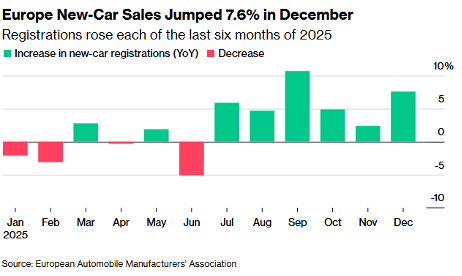

European demand recovery has limited impact on PCTC utilisation

European new-car sales increased for a third consecutive year in 2025, supported by improving consumer sentiment and strong growth in electric and hybrid vehicle registrations. However, this recovery has had a limited direct impact on PCTC demand, as the majority of incremental sales have been supplied by domestic European production rather than long-haul imports. With the exception of select Chinese brands, most notably BYD, European sales growth has not translated into materially higher seaborne vehicle flows, reinforcing that PCTC utilisation remains more closely tied to export-led growth from Asia than to end-market demand within Europe.

Trade policy shifts add incremental upside to demand

January also brought supportive policy developments for PCTC demand. India announced plans to significantly reduce tariffs on imported European vehicles, with an agreement expected to gradually allow up to 250,000 European-made cars to enter the country at preferential duty rates, according to the European Commission. While implementation will be phased, the move is expected to stimulate inbound vehicle flows to India over time and add a new source of demand for long-haul PCTC trades.

Seasonal softness does not alter the structural outlook

Activity eased modestly toward the end of January due to seasonal factors and holiday-related disruptions, but underlying demand conditions remain firm. With vehicle exports expected to continue growing and fleet supply still relatively constrained, PCTC markets enter the remainder of 2026 with a stable utilisation backdrop. January’s developments underscore that export-led demand, supported by both Chinese manufacturing strength and emerging trade policy shifts, continues to define the trajectory of the PCTC segment. Going forward, rapid fleet growth serves as the key risk for the segment.

Sources: Clarksons, Bloomberg, China Association of Automobile Manufacturers, European Commission & Reuters