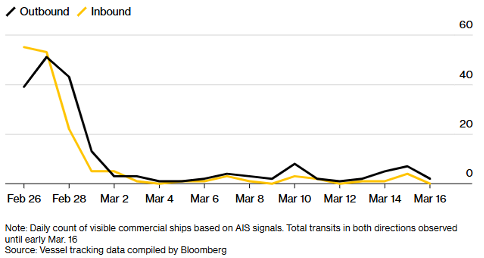

Strikes and vessel attacks drive supply risk as tanker flows stall

This week’s key developments

17 March: Israel conducted strikes on Iran’s South Pars gas field, with U.S. officials stating they had no prior knowledge of the operation.

18 March: Iran retaliated with missile and drone strikes on Qatar’s Ras Laffan LNG hub, with QatarEnergy reporting extensive damage and calling it a “dangerous escalation.”

18 March: Governments proposed a protected maritime corridor as c.20,000 seafarers remained stranded amid halted vessel movements.

19 March: Energy markets moved higher as supply risks intensified across both crude and LNG markets.

The Strait of Hormuz crisis has now escalated into a broader energy conflict, with direct attacks on upstream gas infrastructure compounding existing disruption to shipping. The sequence of strikes, from South Pars to Ras Laffan, marks a clear expansion beyond maritime security into critical production assets, reinforcing the region’s central role in global energy supply. Iran has reportedly targeted around 20 commercial vessels, linked to the U.S., Israel and their allies, underscoring the escalation in maritime risk. At the same time, more than 540 tankers carrying over 300m barrels of oil remain stranded in the Gulf, tightening available supply and amplifying market sensitivity.

From a shipping perspective, transit remains severely constrained. War risk insurances have surged from ~25bps to as high as 3% of vessel value. Pipeline alternatives to the Red Sea have offered limited relief, but the capacity is far lower than usual Gulf exports. With limited safe passage and ongoing security threats, flows through the Strait remain near a standstill. Near term visibility is low, and both freight markets and energy prices are expected to retain a sustained geopolitical risk premium.

Sources: Bloomberg, Reuters & TradeWinds